Copyright © 2026 LP Fintech. All rights reserved.

Blog

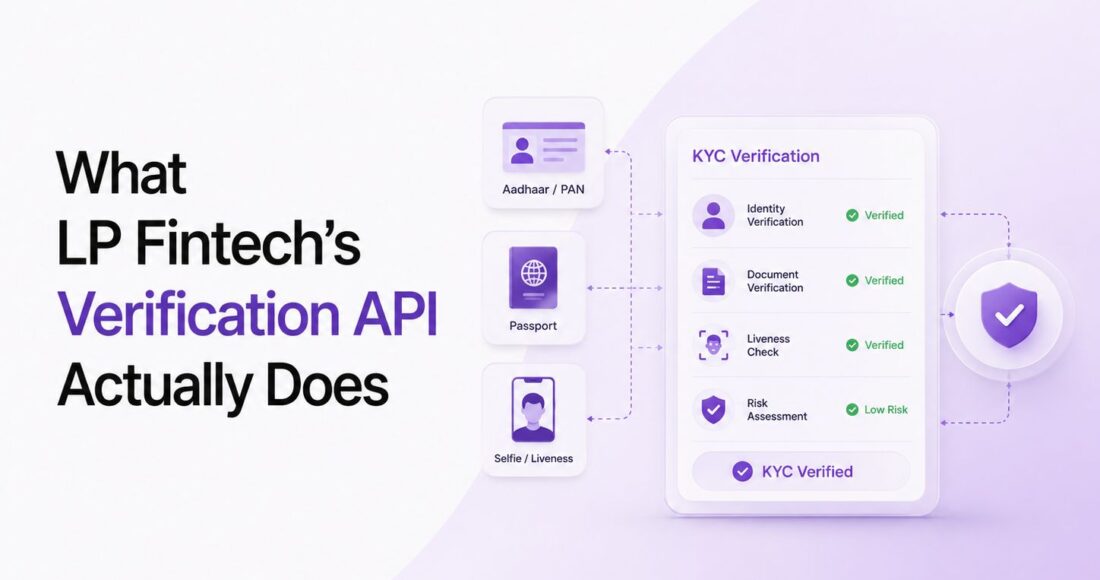

What LP Fintech’s Verification API Actually Does, and Why It Matters for NBFCs

Building a lending product in India involves assembling a verification stack from multiple vendors. Aadhaar from one provider. PAN from another. Bank account verification from a third. Video KYC from a fourth. CKYC fetch from a fifth.

Each vendor has its own API, its own documentation, its own SLAs, and its own support line. When something breaks at 11 PM, it is not always clear which vendor is responsible or how quickly they will respond.

LP Fintech’s Verification Suite was built to consolidate that stack into a single API. Here is what it covers and why each component matters.

Aadhaar Verification

Aadhaar OTP verification and Offline XML verification are both supported. The OTP path is faster for most users. The Offline XML path is useful when the user cannot receive an OTP or when OTP delivery is unreliable due to network conditions. Having both available in the same integration means you can fall back without sending the user to a different flow.

PAN Verification and Name Match

PAN verification is standard. The name match component is where it gets useful. A common onboarding failure point is when the name on a PAN card does not match the name a user has entered in a form, usually because of formatting differences or common name variations. A proper name match algorithm handles these cases rather than returning a hard failure and ending the session.

Bank Account Verification

Penny drop verification confirms account validity by sending a small credit and verifying the response. Pennyless verification does the same without the transaction, making it faster and cheaper for high-volume operations. Both methods are available, and the right choice depends on your volume and the regulatory requirements for your product type.

The practical issue with traditional bank account verification is time. Manual or slow API-based checks can take 24 hours or more. That is a 24-hour gap in an onboarding flow where the user may not come back.

Video KYC

Video KYC is RBI V-CIP (Video-based Customer Identification Process) compliant, which is a requirement for any NBFC or bank using video-based onboarding under RBI guidelines. The key operational consideration is availability. A video KYC service that only works during business hours will generate drop-offs from users who apply in the evening or on weekends. The LP Fintech implementation is available around the clock.

Face Match, Liveness Detection, and OCR

Face match checks the selfie a user takes against their ID document. Liveness detection confirms the user is present in real time, not submitting a photo of a photo. OCR extracts document data automatically, removing the step where users manually type information that is already on their ID.

Each of these reduces friction at a specific point in the onboarding flow. The cumulative effect on completion rates is significant.

CKYC, GST, and Government ID Verification

CKYC (Central KYC Registry) fetch and upload enables re-use of verified KYC data from the central registry, reducing the need for repeat verification for users who have already been KYC’d elsewhere. GST/GSTIN lookup verifies business entity details for B2B or MSME lending products. Voter ID and Driving Licence verification round out the government ID coverage.

The Case for a Unified Stack

Each component in this stack solves a specific failure point. Taken together, they cover every major reason an onboarding session fails before the user reaches the loan application or account activation step.

The argument for a unified API is not just about convenience. It is about accountability. With a single provider, there is one integration to maintain, one place to look when something breaks, and one SLA to hold someone to. For NBFCs and fintech platforms operating at scale, that operational simplicity has real value.